Owning a home is a dream for millions of families in Pakistan. Yet for many people, rising property prices and construction costs make this dream difficult to achieve. With housing demand increasing every year, a large number of families continue to live in rented homes or shared accommodations.

Pakistan currently faces a housing shortage estimated at nearly ten million housing units.

To address this challenge, the government introduced the Mera Ghar Mera Ashiana Scheme. The initiative is designed to provide affordable housing financing and help people either build or purchase their own homes.

What is the Mera Ghar Mera Ashiana Scheme?

The Mera Ghar Mera Ashiana Scheme is a low cost housing scheme launched to assist the low and middle income families with access to subsidized home financing at reduced rates. The program supports both house construction and property purchase by offering long term loans through commercial banks.

The scheme operates under the guidance of the State Bank of Pakistan. With this program qualified applicants are able to get financed small houses or apartments with easy terms of repayment and government backed subsidies.

Purpose of the Mera Ghar Mera Ashiana Scheme

The scheme was introduced to address several important challenges related to housing and economic development.

Reducing Pakistan’s Housing Shortage

There has been a major shortage of residential units in Pakistan. The rapid population explosion and urban migration has also necessitated housing especially in the big cities. The affordable housing schemes like the Mera Ghar Mera Ashiana Scheme assist in decreasing this disparity by promoting new buildings and making houses affordable to the larger population of families.

Supporting Low and Middle Income Families

Providing homes that are unaffordable by households with high costs of loans is one of the primary goals of the program. The scheme enables individuals that have modest incomes to own property by providing subsidized financing and reduced profit rates.

Boosting the Construction Industry

Housing development makes numerous other sectors of the economy lively. Additional building can lead to the need of building materials in form of cement, steel, bricks and electrical supplies.

Encouraging Home Ownership

Ownership of homes offers financial stability to the family in the long term. The homeowners accumulate property equity as they work on their property improvement but pay rent over years as they improve their living standards.

Who is the Mera Ghar Mera Ashiana Scheme For?

The program is specifically designed for people who struggle to access conventional housing loans.

Low Income Families

Limited income of households per month does not always allow paying high mortgage payments. The scheme provides low-cost financing that can afford such families home ownership.

First Time Home Buyers

Others have the land but they are not able to put up a house due to the lack of funds. The scheme financing of construction assists them to construct homes on their current plots.

Individuals Who Own Land but Cannot Afford Construction

Some people already have land but lack the funds needed to construct a house. Construction financing under the scheme helps them build homes on their existing plots.

Types of Houses Covered Under the Scheme

The program focuses on affordable housing units with specific size and financing limits.

Category | Property Size | Maximum Financing |

Tier 1 | Up to 5 Marla house or apartment | Up to PKR 2 million |

Tier 2 | Up to 10 Marla house | Up to PKR 6 million |

Tier 1 typically targets low income families who require smaller housing units.

Tier 2 provides slightly larger financing options for middle income applicants.

Both categories allow financing for either purchasing a house or constructing one on owned land.

Financing Limits and Loan Amount

Financing under the scheme depends on the applicant’s income, property value, and bank policies.

Typical financing features include:

Loan amounts designed for small residential houses

Partial government subsidy on markup rates

Flexible repayment option

Financing for both house purchase and construction

Banks usually require applicants to contribute a small portion of the total property cost. This ensures shared responsibility between the borrower and the lender.

Financing Duration and Repayment Period

A major advantage of the scheme is its long repayment period.

Applicants can choose financing durations such as:

10 years

15 years

20 years

25 years

Profit Rates and Government Subsidy

The government provides a subsidy to make housing loans more affordable.

Below is a simplified overview of the markup structure.

Loan Period | Estimated Markup Rate |

First 5 years | Around 3% to 5% |

Remaining period | Approximately 7% to 9% |

All housing financing programs under this initiative operate under the regulatory supervision of the State Bank of Pakistan.

Banks Offering the Mera Ghar Mera Ashiana Scheme

Several commercial banks participate in the housing financing program. These banks evaluate applications and provide loans according to the scheme’s guidelines.

Participating banks include:

National Bank of Pakistan

Bank of Punjab

Meezan Bank

Bank Alfalah

Habib Bank Limited

MCB Bank

Allied Bank

Each bank may have slightly different documentation requirements and evaluation procedures.

Eligibility Criteria for the Scheme

To qualify for financing under the Mera Ghar Mera Ashiana Scheme, applicants must meet certain requirements.

Common eligibility criteria include:

Applicant must be a Pakistani citizen

Minimum age requirement usually starts at 21 years

Applicant must have a stable source of income

The property must fall within the scheme’s size limits

Applicant should not have a history of loan default

Valid CNIC must be provided

Both salaried employees and self employed individuals can apply if they can demonstrate financial stability.

Required Documents

Applicants are typically required to submit the following documents.

Copy of CNIC

Proof of income such as salary slips or business income statements

Recent bank statements

Property ownership documents or purchase agreement

Passport size photographs

Utility bills for address verification

Banks may request additional documents depending on the nature of the application.

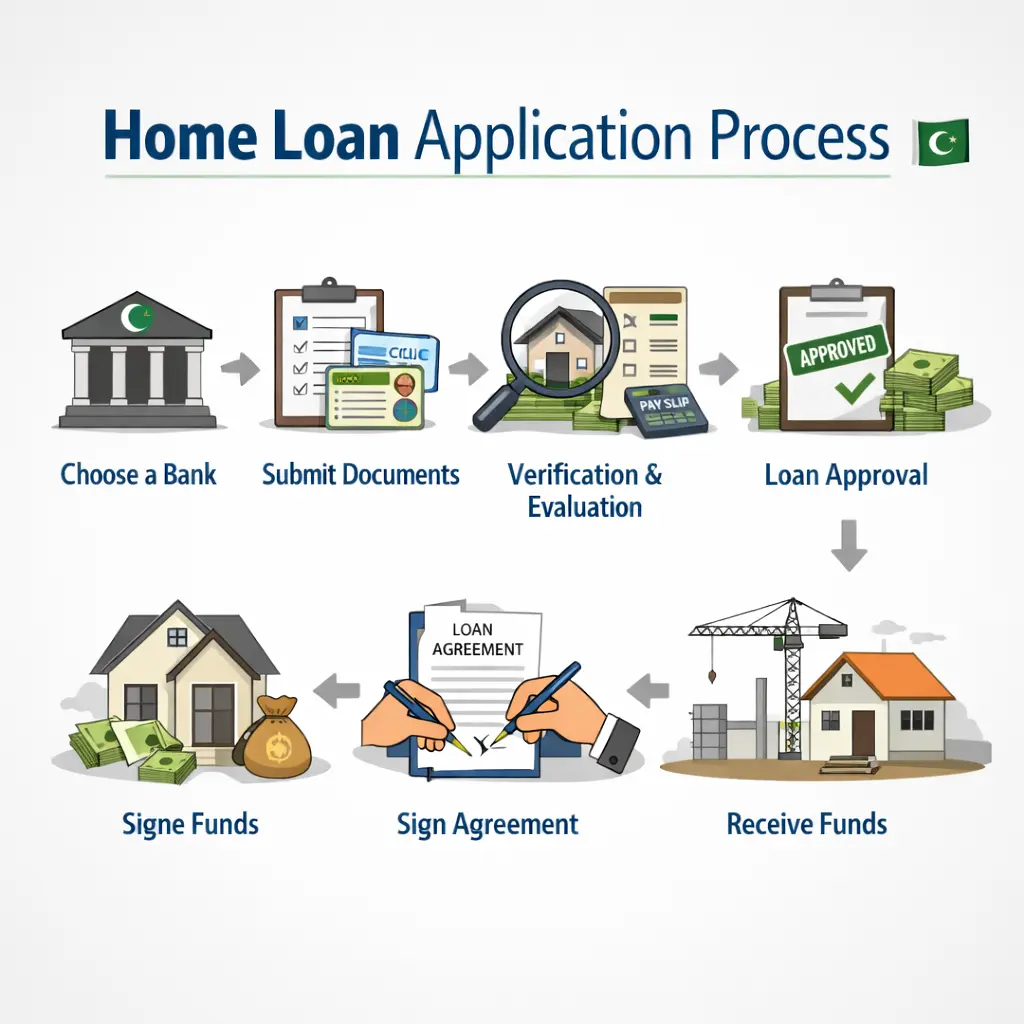

Step by Step Application Process

The application process generally follows these steps:

Choose a participating bank that offers the housing finance program.

Submit the application form along with required documents.

The bank reviews income records and verifies property details.

Financial evaluation is conducted to determine loan eligibility.

Once approved, the bank issues financing terms and conditions.

After agreement signing, the financing amount is released for property purchase or construction.

Application Deadline and Availability

Many housing finance programs remain open until the allocated subsidy funds are fully utilized. Instead of a fixed deadline, banks typically continue accepting applications as long as the financing quota remains available.

Interested applicants should check with participating banks to confirm current availability.

Benefits of the Mera Ghar Mera Ashiana Scheme

The program offers several advantages for individuals planning to own property.

Key benefits include:

Affordable financing options

Government supported markup subsidy

Long repayment duration

Opportunity to build or purchase a home

Improved access to housing for low income families

Growth in construction and related industries

These benefits make the scheme an important step toward improving housing accessibility in Pakistan.

Important Tips Before Applying

Before applying for housing finance, applicants should consider several factors.

Maintain a good credit history with banks

Ensure property documents are authentic and verified

Plan construction budgets carefully

Understand loan repayment terms clearly

Taking time to evaluate these factors can help applicants avoid financial difficulties in the future.

Planning to Build Your Home After Loan Approval?

Several borrowers prefer the construction funding as a way of constructing their houses on the land they have. Nevertheless, a house is a construction that demands proper planning, budgeting and materials.

It can be easier and more effective when it comes to selecting construction partners that can be trusted. GharHub is a professional construction company that provides homeowners with guidance on construction project planning, cost estimation, and choice of building materials that are long lasting.

FAQ’s

Q1. What is the Mera Ghar Mera Ashiana Scheme?

Housing finance program of a government, which assists low and middle income families to purchase or construct homes with the help of banks under the control of State Bank of Pakistan.

Q2. Who can apply?

Pakistani nationals who have valid CNIC, earn a stable income without default of a loan.

Q3. What is the loan limit for the Mera Ghar Mera Ashiana Scheme?

Maximum PKR2 million on 5 Marla homes and PKR 6 million on 10 Marla homes.

Q4. Which banks offer it?

Banks like National Bank of Pakistan, Bank of Punjab, Meezan Bank, and Bank Alfalah.

Q5. How to apply?

Banks such as National Bank of Pakistan, Bank of Punjab, Meezan Bank and Bank Alfalah.